Navigating Your Balance Sheet in a Falling Rate Environment

March 26, 2024

Overview

In the wake of a tumultuous 2023 that featured the most aggressive rate hiking cycle in nearly 36 years, the economic outlook has started to shift. And while the risk of a recession still looms, there remains a path toward an economic soft landing. Although it is not definitive as to when, Federal Reserve (Fed) Chair Jerome Powell and the Federal Open Market Committee (FOMC) have indicated plans to measure and respond to economic data as it becomes available and have forecasted an easing of rates at some point this year. Based on the Summary of Economic Projections from the meeting on March 20, 2024, FOMC participants see approximately three 25 basis point (bps) cuts in 2024 (or 0.75%), based on their individual assessment of appropriate monetary policy. According to interest rate traders, there is currently a greater than 60% chance of the first rate cut occurring at the June FOMC meeting.

Inflation, while still elevated, has subdued. Combined with stronger than expected jobs, housing, and gross domestic product (GDP) readings, it appears the Fed’s work is paying dividends as the likelihood of a soft-landing becomes more probable by the day. Whether the U.S. economy falls into a recession or not, the expectation that rates will come down this year makes it imperative for members to consider how to manage their balance sheet in a falling rate environment.

Balance Sheet Trends and Betas

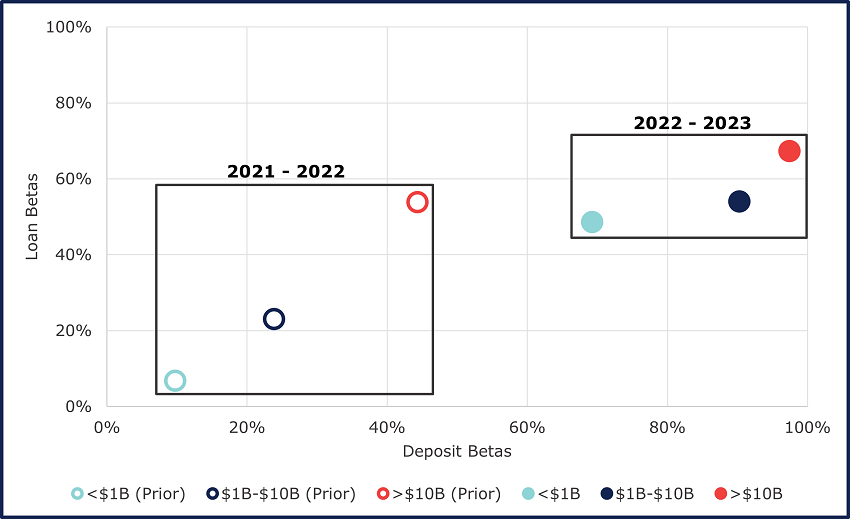

Over the past two years, FHLBank Chicago members have felt elevated pressure from increasingly rate sensitive depositors, which is reflected by the shift in deposit composition and higher percentage of interest-bearing deposits on balance sheet. As evidenced by the chart below, members across all asset sizes have reacted to the rapid rate hiking cycle and pressure from depositors by increasing deposit betas. This shift has resulted in net interest margin (NIM) compression as loan betas have fallen behind.

Source: S&P Global, FHLBank Chicago Member Cost of Interest-Bearing Deposits & Yield on Loans & Leases (23Q4, 22Q4, 21Q4). Regression run against the 2023 Q4 Avg. EFFR of 5.33% & 2022 Q4 Avg. EFFR of 3.64%, and 2021 Q4 Avg. EFFR of 0.07% (New York Fed).

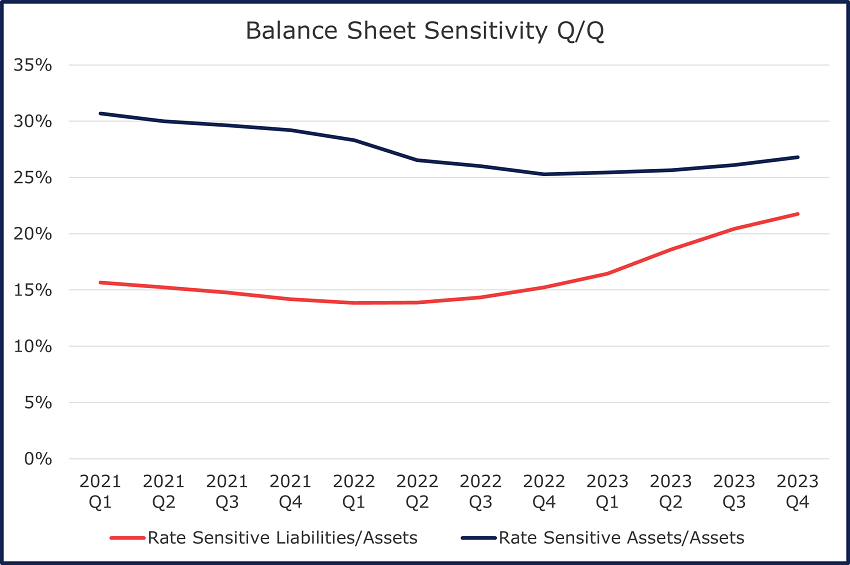

As we approach the end of the hiking cycle and start considering rate cuts, members have seemingly started to re-position their balance sheets for such a shift by increasing their proportion of rate sensitive liabilities over the past several quarters. While holding a higher percentage of floating rate liabilities may pressure NIM in the short-term as rates remain elevated, it also presents an opportunity to benefit from falling rates in the medium- to longer-term.

Source: S&P Global, FHLBank Chicago Member Rate Sensitive Assets/Assets, Rate Sensitive Liabilities/Assets (23Q4 vs. 22Q4), Gap/Assets (2023 vs. 2022)

Managing Balance Sheet Sensitivity

Although not all institutions are created equal, it is crucial to have a properly hedged balance sheet that takes multiple economic outcomes into consideration. An asset-sensitive balance sheet is one where the institution’s assets reprice more quickly than its liabilities. In such a scenario, net interest income (NII) tends to move in the same direction as interest rates, increasing when rates rise and decreasing when rates fall. A liability-sensitive balance sheet is the opposite, and one where the institution’s liabilities reprice more quickly than its assets. In this scenario, NII tends to move in the opposite direction as interest rates, increasing when rates fall and decreasing when rates rise.

Whether your balance sheet is more asset or liability sensitive, measures can be taken to ensure proper positioning for expected changes to interest rates or an unexpected rate shock. Additionally, it is important to monitor the optionality risk of your assets and liabilities, and how the exercise of those options can affect the sensitivity of your balance sheet. For example, customers prepaying mortgages early and/or customers unexpectedly withdrawing their deposits.

Decreasing Asset Sensitivity and Increasing Liability Sensitivity in a Falling Rate Environment

It's important for both asset- and liability-sensitive institutions to strike a balance between optimizing interest income and the pursuit of yield with the management of potential downside risks associated with interest rate fluctuations. Maintaining and continually updating your asset and liability management (ALM) models, understanding depositor behavior, and having multiple liquidity outlets are a few key considerations when hedging risk, but the choice of strategies will depend on your institution’s risk tolerance, market conditions, and long-term strategic goals.

Extend Asset Duration: Extend the maturities of assets to capture higher yields on longer-term, fixed-rate investments.

Focus on Fixed-Rate Assets: Increase the proportion of fixed-rate assets in your portfolio to lock in higher yields before rates decline further. Consider investing in longer-term fixed-rate securities, such as government bonds or mortgage-backed securities. While security portfolios have taken a hit over the past year, the opportunity to recoup losses still exists in our high-rate environment.

Interest Rate Swaps on Floating Rate Loans: Utilize receive-fixed interest rate swaps to convert floating-rate loans into fixed-rate assets, helping to stabilize interest income as rates fall.

Adjustable-Rate Loans With Embedded Floors: If you originate adjustable-rate loans, including an embedded interest rate floor will ensure a minimum level of interest income even if rates fall lower than expected.

Shorten Liability Duration: Shorten your liability duration by staying short on the curve and using floating rate advances, allowing your liabilities to reprice as rates fall, decreasing interest expense.

Interest Rate Swaps on Fixed Rate Advances: Utilize receive-fixed interest rate swaps to convert fixed-rate FHLBank advances into floating-rate exposure, helping to shorten the duration of your liabilities and decrease interest expense as rates fall.

Other Considerations:

Refinancing Risk: Institutions may face higher demand for loan refinancing as borrowers take advantage of lower rates, leading to prepayments, refinances, and potential loss of income from interest-bearing assets.

Asset/Liability Matrix:

Advance Strategies

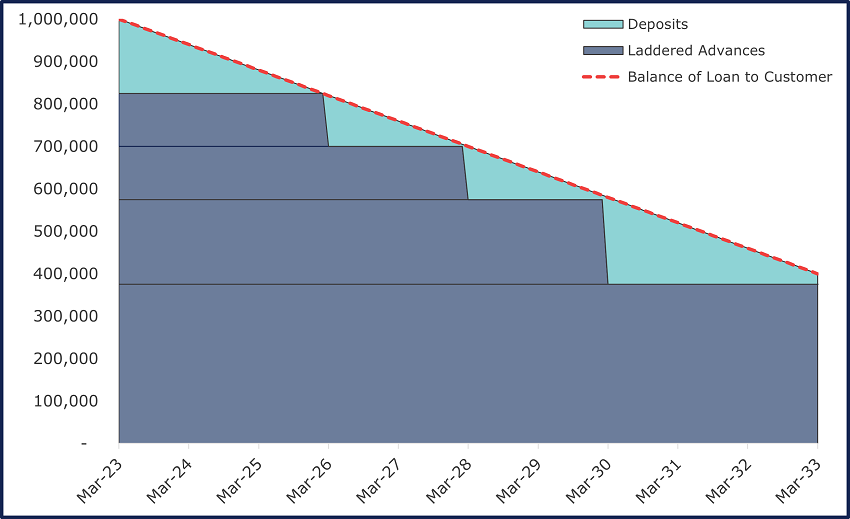

Short-Term, Fixed-Rate Advances: Members can take advantage of falling interest rates by using short- or medium-term fixed-rate advances. A ladder of these advances can provide a more predictable funding cost than floating rate advances, shielding institutions from daily rate fluctuations while also allowing members to finance into lower rates as the shorter-term advances mature. A combination of short- and medium-term advances will allow you to have flexibility in your funding strategy should rates vary from the forecasted path.

If rates remain elevated for longer than anticipated, the inclusion of medium-term advances in your advance ladder allows you to benefit from the inverted yield curve since those advances will have been priced lower based on the forward curve at that time.

Amortizing Advances: Amortizing advances can be used to hedge risk expose as the advance features scheduled principal repayments over the loan term. While normally used to match fund amortizing loans, these advances can also help manage interest rate risk by helping back gradually reduce higher cost funding exposure as interest rates decline and deposit inflows increase. If rates fall faster than anticipated, the short-term advances will reprice closely with the market. Amortizing advances can be structured to best suit your needs, including customized principal repayment schedules.

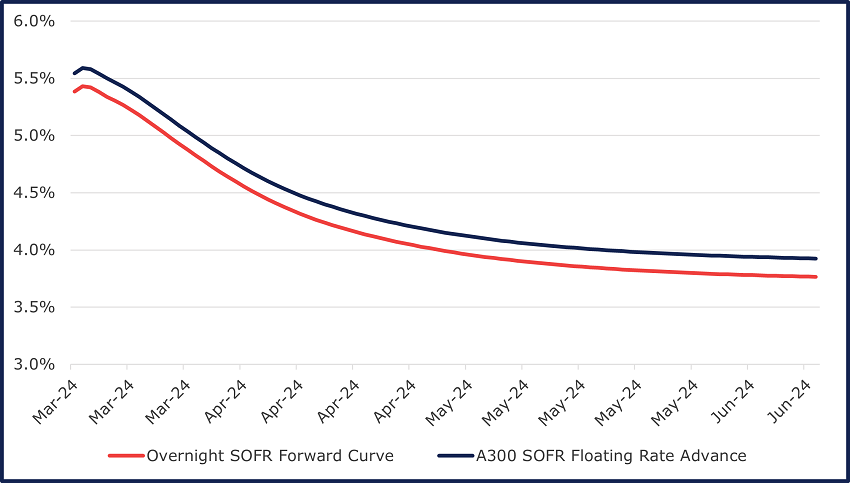

Floating Rate Advances: Floating rate advances can be an excellent source of funding for members who anticipate lower rates in the future. Indexed to Secured Overnight Financing Rate (SOFR), Federal Home Loan Bank Discount Notes, the federal funds rate, or prime, floating rate advances can be used to match fund floating rate assets to lock in a desired NIM for the duration of the asset. Additionally, floating rate advances can be used for general funding purposes to reduce liability duration which would benefit NIM if rates decline since the advance would continue to reset lower with market rates.

Source: FHLBank Chicago historical advance rates, Overnight Forward SOFR Curve

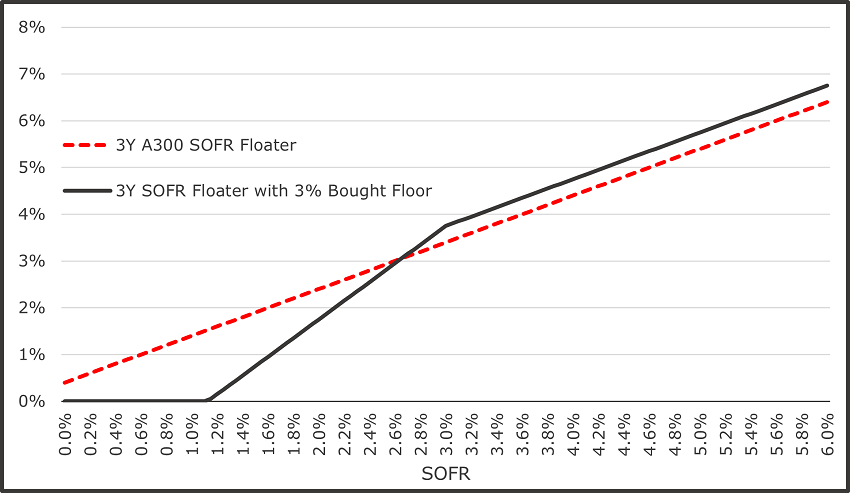

Floating Rate Advance With Embedded Floor*: As further protection in a falling rate environment, members can purchase and embed an interest rate floor into a floating rate advance indexed to SOFR. If SOFR falls below the member selected floor strike rate, the advance rate will decline at a rate of 2:1, or twice as fast as SOFR. With the market value of the advance increasing below the strike, this advance can be particularly helpful for hedging assets whose market value declines as rates fall.

*Currently in-development, expected to be available Q2 2024

Short-Term Putable Fixed Rate Advances: Putable fixed rate advances, when used appropriately and with full understanding of the risks, can be an effective funding option for members looking to reduce their cost of funds. Putable advances are an option-embedded advance where the member sells FHLBank Chicago the option to prematurely “put” or terminate the advance prior to the advance’s stated maturity date. The premature termination by the FHLBank Chicago may only occur after the agreed upon lockout period (the period when the advance cannot be terminated by FHLBank Chicago) and only on certain, agreed-upon termination dates thereafter. In return for selling the option, members receive a below-market interest rate.

We offer both European (Euro) and Bermudan (Berm) option types which determine how frequently FHLBank Chicago has the option to terminate the advance. A European option provides a one-time option to terminate the advance at the end of the lockout period. A Bermudan option provides the option to terminate the advance at the end of the lockout period, and at periodic dates thereafter (e.g., quarterly).

One of the key risks associated with putable advances is duration risk. As rates fall, extension risk (the risk that the advance is not terminated early and extends to its full maturity date) becomes a consideration. In this situation, the advance may remain outstanding longer than the member had expected which could lead to an asset liability mismatch. Conversely, in a rising rate environment, contraction risk (the risk that the advance is terminated prior to its maturity date) becomes a consideration. While the interest rate of the putable advance relative to market interest rates is a component of whether FHLBank Chicago will decide to terminate the advance early, FHLBank Chicago cannot and does not make any representations as to the expected life of a putable advance nor the specific criteria that may cause the Bank to exercise its option. Depending on your view of the forward curve and rate expectations, putable advances with shorter final terms and short lockout periods offer attractive funding relative to standard fixed rate advances.As further protection in a falling rate environment, members can purchase and embed an interest rate floor into a floating rate advance indexed to SOFR. If SOFR falls below the member selected floor strike rate, the advance rate will decline at a rate of 2:1, or twice as fast as SOFR. With the market value of the advance increasing below the strike, this advance can be particularly helpful for hedging assets whose market value declines as rates fall.

| Term | Lockout Period | Putable Rate | 6 Month Fixed Rate | Spread to Comparable Advance |

|---|---|---|---|---|

| 1 Year | 6 Month (Berm) | 5.30% | 5.58% | -0.28% |

| 1 Year | 6 Month (Euro) | 5.32% | 5.58% | -0.26% |

| 2 Year | 6 Month (Berm) | 4.62% | 5.58% | -0.96% |

| 2 Year | 6 Month (Euro) | 4.75% | 5.58% | -0.83% |

Takeaways

It’s crucial to be prepared for multiple scenarios and unexpected outcomes given our dynamic environment and the influence of many factors including geopolitical, financial, and regulatory, amongst others.

While the expectation of rate cuts has been at the focal point for the past few months, it’s always wise to be prepared for different challenges that could positively or negatively affect your balance sheet including rates staying higher for longer and/or fewer cuts than anticipated. To navigate the current market, it’s imperative to sustain proper ALM management, employ appropriate hedge strategies, and utilize the resources at your disposal to help manage your balance sheet. In times like these, the FHLBank Chicago is here to serve you as a trusted advisor for your institution’s balance sheet and funding requirements.

To Learn More

If you are an FHLBank Chicago member and want to discuss potential funding options and balance sheet strategies, please contact your Sales Director or email solutions@fhlbc.com.

Download a PDF of this white paper.

Contributors

|

| |